Related Articles

A new amnesty law has been introduced in Turkey that allows for settlement of existing tax liabilities and immunity against a potential tax audit for individual taxpayers.Turkey’s Law number 6111 (referred to as the “Tax Amnesty law”) was published in the official gazette (Resmi Gazete) on 25 February 2011, and entered in to force on the same day.

A new amnesty law has been introduced in Turkey that allows for settlement of existing tax liabilities and immunity against a potential tax audit for individual taxpayers.Turkey’s Law number 6111 (referred to as the “Tax Amnesty law”) was published in the official gazette (Resmi Gazete) on 25 February 2011, and entered in to force on the same day.

This Flash International Executive Alert aims to provide general insight and explain the provisions of the Tax Amnesty law affecting individual taxpayers only.

Covered Periods of Tax Liabilities

- Tax returns submitted until 31 December 2010, for taxes declared through the tax return and related tax penalties and late payment interest charges.

- Taxes accrued before 31 December 2010, and related tax penalties and late payment interest charges.

- Tax penalties, which are not related to tax principal amounts, applied for the period before 31 December 2010.

Requirements for Benefitting from Tax Amnesty

The requirements which must be satisfied in order to benefit from the provisions of the Law are as follows:

- A written application to the tax office, which can be submitted until the end of the second month following the month in which the Tax Amnesty law is enacted.

- The withdrawal of any open lawsuits by the taxpayer and a pledge not to pursue other legal actions or administrative redress (in relation to the taxpayer’s outstanding liabilities).

- During the implementation period, tax and “premium” payment obligations for the current periods should be met.

Voluntary Tax Base Increases

One of the most important provisions introduced by the Tax Amnesty law is the application of the so-called Voluntary Tax Base Increase which enables taxpayers to “close” their accounts against a tax audit related to the years and type of taxes for which they have made a tax amnesty application (which otherwise remain ”open” for a tax audit for the last five years).

According to the Tax Amnesty law, those taxpayers who voluntarily increase their tax bases in respect of the years 2006, 2007, 2008, and 2009, at a rate determined by the Tax Amnesty law, and thus pay a certain amount of additional tax related to those years, will effectively be granted immunity against a potential tax audit related to the years and type of taxes for which they have made a tax amnesty application. Please note that the above-mentioned provision does not cover the year 2010.

Taxes that are due following the tax base increase can be paid either in a single lump sum installment or in 6, 9, 12, or 18 installments over a period of 12 to 36 months with a fixed-rate interest applied based on the number of installments.

The application for the voluntary tax base increase needs to be filed with the authorities – taxpayers have until 2 May 2011 to do so.

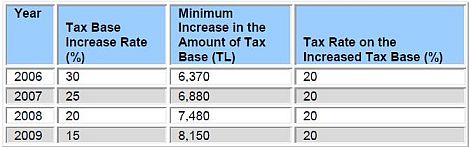

Tax Base Increase in Individual Income Tax – for Income other than Business and Professional Services Income (e.g., Income Taxes on Salary Income)

The minimum increase in the amount of the tax base, as shown above, will alternatively apply if there is no tax base in that year due to deductions, exemptions, etc.

Please note that individual taxpayers who have failed to file their income tax declarations in the relevant periods can still benefit from the Tax Amnesty by claiming the above-mentioned minimum tax base and effecting payment of a 20-percent tax on this amount.

Rules Related to a Taxpayer’s Liabilities When Subject to the Tax Audit and/or Assessment Stage

Tax audits that have already commenced before the date of enactment of the Tax Amnesty Law will be continued until the final assessment and accrual phases, and after finalization of these phases, the following will apply:

- Taxpayer will be required to pay 50 percent of the principal tax assessed as a result of the tax audit (i.e., the remaining 50 percent will be written off).

- The potential tax penalties and late payment interest charges related to the assessment shall not be applied, but the payable amount (i.e., 50 percent of the principal) will be increased by the inflation index.

- The resulting amount has to be paid in six (6) installments over the course of 12 months following the date of assessment.

- All remaining tax penalties, late payment interest, and similar charges, will be removed.

Footnote:

1 Law number 6111 in respect of the settlement of fiscal liabilities, the increase of previous years’ tax bases, the restructuring of tax and other public receivables, and the declaration of certain out-of-book assets and transactions (6111 Sayılı Bazı Alacakların Yeniden Yapılandırılması ile Sosyal Sigortalar ve Genel Sağlık Sigortası Kanunu ve Diğer Bazı Kanun ve Kanun Hükmünde Kararnamelerde Değişiklik Yapılması Hakkında Kanun; 25 Şubat 2011 Tarihli ve 27857 Sayılı Resmî Gazete – Mükerrer ile yayimlandi). For the Resmi Gazete, see: http://resmi-gazete.org